Power of Sale in Ontario: What Buyers, Sellers, and Investors Actually Need to Know in 2026

Power of Sale in Ontario: What Buyers, Sellers, and Investors Actually Need to Know in 2026

The 35-day window most homeowners don't know they have — and the risks most buyers don't ask about before they write an offer.

I've had three separate conversations this month with people who used "power of sale" and "foreclosure" interchangeably. They're not the same thing, and mixing them up costs people money — whether you're the homeowner behind on payments or the buyer eyeing a "motivated seller" listing on Realtor.ca.

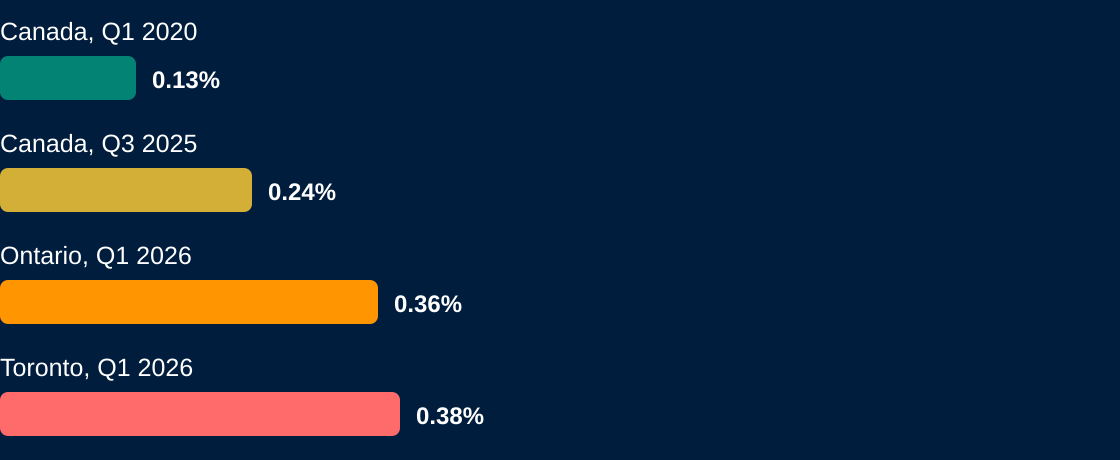

In 2026, Ontario's 90+ day mortgage delinquency rate climbed to roughly 0.36%, up about 52% year over year (CMHC, Q1 2026). It's still low by historical standards, but it's the steepest climb in years, and it's pulling more power of sale listings into the resale market across Waterloo Region, the GTA, and South-West Ontario. So let's get the mechanics right.

Key Takeaways

- Ontario's 90+ day mortgage delinquency rate hit ~0.36% in Q1 2026, up 52% year over year (CMHC), with a national peak near 0.30% projected by mid-2026.

- Under the Mortgages Act, a lender must wait at least 35 days after serving a Notice of Sale before selling — and the homeowner can redeem (pay the arrears) right up until closing.

- Power of sale isn't foreclosure. The homeowner keeps any surplus, but also stays on the hook for any shortfall.

- Power of sale homes sell "as is, where is" — no Seller Property Information Statement, no warranties on the roof, furnace, or appliances.

What Does Power of Sale Actually Mean in Ontario?

Power of sale is a clause baked into virtually every Ontario residential mortgage that lets a lender sell a property after the borrower defaults, without going to court first. As of 2026, it's the dominant default-recovery route in this province — lenders use it instead of foreclosure because it's faster, cheaper, and doesn't require them to take ownership of the home (RBHF, 2026).

Here's the part that surprises most people: during a power of sale, the homeowner is still the legal owner of the property right up until closing day. The lender gains the right to sell, not the title. That single distinction explains nearly every other difference between power of sale and foreclosure.

Curious what your home is actually worth right now? Get a free home evaluation before you make any decisions.

Power of Sale vs. Foreclosure: The Difference That Actually Matters

A power of sale is a lender exercising a contractual right to sell; a foreclosure is a court order that extinguishes the borrower's ownership entirely and transfers title to the lender (RBHF, 2026). In foreclosure, any equity above the mortgage balance goes to the lender. In power of sale, the homeowner is entitled to the surplus once the lender, the legal fees, and the arrears are paid out.

The trade-off cuts both ways. In a foreclosure, the debt is considered settled by the property itself — the lender can't come back for more. In a power of sale, if the home sells for less than what's owed, the lender can sue the former owner for the shortfall as an unsecured debt (Hoyes Michalos, 2026).

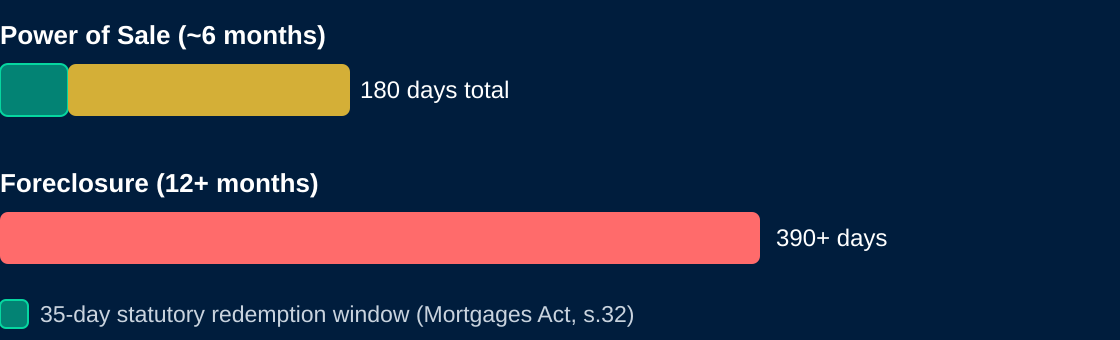

Illustrative comparison of typical Ontario timelines. Source: RBHF, "The Difference Between Foreclosure and Power of Sale in Ontario," 2026.

Most lenders in Ontario don't even bother with foreclosure anymore. It's slower, it costs more in legal fees, and it forces the bank to carry and manage a property it doesn't want. Power of sale lets them get their money back and move on.

The Power of Sale Timeline: Why 35 Days Matters More Than People Think

Under section 32 of Ontario's Mortgages Act, a lender can't serve a Notice of Sale until the borrower has been in default for at least 15 days — and once that notice is served, the sale itself can't happen for at least 35 days (40 days if the property is occupied by a married couple, or for commercial properties). That window is the redemption period, and the lender is legally barred from taking further enforcement steps while it's running.

During the redemption period, paying the arrears, costs, and accrued interest in full reinstates the mortgage and stops the sale (Cactus Law, 2026). Even after that window closes, the right to redeem generally runs until the transaction actually closes — which is why every power of sale purchase agreement in Ontario carries genuine "the deal could fall through" risk for the buyer, right up to the closing table.

What Happens to the Money: Surplus, Deficiency, and Your Credit Score

When a power of sale closes, the proceeds get paid out in order: legal and selling costs first, then the outstanding mortgage balance plus interest and arrears, then any subordinate mortgages or liens, and only then does whatever's left — the surplus — go back to the former homeowner. If the sale price doesn't cover the debt, the gap becomes a deficiency the lender can pursue as an unsecured claim against the borrower's other assets or income (Hoyes Michalos, 2026).

The credit damage is real and it's not short-lived. A power of sale can drop a credit score by roughly 100 to 160 points depending on prior history, and the record stays on file for up to seven years (Power of Sale Ontario, 2026). That's a long shadow over your ability to get approved for a new mortgage, a car loan, or in some cases a job that runs a credit check.

Source: CMHC, Mortgage Delinquency Rate (Canada, Provinces, CMAs), Q1 2026.

If You're Behind on Payments: Your Options Before It Gets to This Point

Every homeowner I've worked with who got a Notice of Sale waited too long to make the first call. Not to the lender — to me, or to a lawyer, or to a mortgage broker. By the time someone reaches out in week three of the redemption period, the options have already narrowed.

If you're behind, here's the order I'd work through, first to last:

- Call the lender first. Most are open to a temporary payment plan or short forbearance, especially if the default is recent and resolvable (Rabideau Law, 2026).

- Refinance if you have equity. A new first mortgage, or a second mortgage to cover the arrears, can buy time — especially through a private lender if your credit has already taken a hit.

- List the home yourself, before the lender does. A voluntary sale gives you control over price, timing, and showings, and it almost always nets more than a forced sale on a lender's clock.

- Talk to a licensed insolvency trustee. A consumer proposal can sometimes restructure unsecured debt enough to free up room to keep current on the mortgage.

The redemption period exists precisely so homeowners have room to do one of these things. Use it early — not as a last resort in week 30.

Behind on payments? Don't wait for week 30.

Every option above gets weaker the longer you wait. A 15-minute call costs nothing and tells you exactly where you stand.

Buying a Power of Sale Property: What the Listing Photos Don't Show You

The misconception I run into most with buyers isn't about the legal process — it's the assumption that a power of sale listing is a steal. Sometimes it is. More often, the discount reflects real risk that the price is compensating you for, not a market inefficiency you've stumbled onto.

Power of sale properties sell on an "as is, where is" basis. The lender strips out the standard representations and warranties you'd expect in a normal resale (Kormans LLP, 2026). There's no Seller Property Information Statement, because the seller — the bank — has never lived in the house and knows nothing about its history. No one's warranting that the furnace works, that the roof doesn't leak, or that there isn't an open work order with the municipality.

▲ If You're Selling / Behind

- You keep title and leverage until closing

- You're entitled to any surplus after the sale

- Redemption, refinance, or a voluntary sale can all still work

- Acting in week one beats acting in week thirty

⚠ If You're Buying

- No Seller Property Information Statement

- No warranties on furnace, roof, or appliances

- Deal can fall through if the owner redeems before closing

- Financing and insurance need confirming early

A few things I tell every buyer before they write an offer on one of these:

- Budget for a full inspection and a contingency fund. You're buying without disclosure, so treat the inspection as your only line of defence.

- Confirm financing and insurability before you waive conditions. Some lenders and insurers are cautious about as-is properties — sort this out early.

- Check for work orders and outstanding liens. Title and municipal searches matter more here than on a typical resale.

None of that means avoid these listings. It means go in with your eyes open and a team — lawyer, inspector, mortgage broker — who's done this before. Curious what's currently available? Search current listings, including power of sale properties in your area.

Why Power of Sale Listings Are Showing Up More Often in 2026

This isn't happening in a vacuum. CMHC has flagged that arrears typically surface six to twelve months after a mortgage renewal, and 2026 is a heavy renewal year for the wave of mortgages originated during the low-rate 2020–2021 period (CMHC Residential Mortgage Industry Report, Spring 2026). Real estate professionals across the GTA are reporting more power of sale activity coming onto the market as a result, even though, as CMHC notes, delinquency rates remain low by historical standards (Yahoo Finance Canada, 2026).

What this means locally: don't be surprised to see more as-is, distressed, and power of sale listings mixed into the regular inventory across Kitchener, Waterloo, Cambridge, and the broader Halton-Peel-Guelph corridor through the rest of 2026. For sellers and buyers alike, it's a reason to know this process cold rather than learn it on the fly during a transaction.

Want the bigger market picture? Read the April 2026 Real Estate Market Update for Waterloo Region, Halton, Peel & Guelph.

Frequently Asked Questions

Is power of sale the same as foreclosure in Ontario?

How long does a power of sale take in Ontario?

Can I still stop a power of sale after I get the notice?

Is buying a power of sale home in Ontario a bad idea?

Does a power of sale hurt my credit score?

Bottom Line

Power of sale isn't a death sentence for homeowners, and it isn't a guaranteed bargain for buyers — it's a process with specific rules, real timelines, and real money at stake on both sides. If you're behind on your mortgage, the redemption period is your window to act, and the earlier you use it, the more options you keep. If you're eyeing a power of sale listing, the discount is paying you for the due diligence the bank won't do. Make sure you actually do it.

Facing a Notice of Sale — or eyeing a power of sale listing?

Get a straight answer in 15 minutes, not 15 days. No pressure, no obligation — just the facts for your specific situation.

Recent Posts